Information hub

All the latest views and news here

A Student’s Guide to Project Development & Finance

I. OVERVIEW OF PROJECT DEVELOPMENT & FINANCE

Project development & finance (PDF) involves the development and long-term financing of infrastructure and industrial projects. There are several differences between project financing and regular financing which can, broadly speaking, be broken down in the following heads:

(a) Timescale: compared to the fast turnaround of most regular financings which take a few months from start to finish, the average turnaround of a project financing is five years. Particularly in the case of infrastructure projects, such as the ones Shearman & Sterling is usually involved in, the projects often span decades.

(b) Cash flows: compared to regular financing which is based on the finances of the sponsors, project financing is based upon the future cash flows of the project.

(c) End product: compared to the immaterial nature of regular financing transactions, project financing has a tangible end-product, often in the form of infrastructure projects which in many cases are helping countries drive economic growth.

2. MAIN PARTIES

Lenders

The lenders are the investors who provide the debt portion of the project financing. The sheer size of a typical project financing deal means that most lending cannot be undertaken by a single lender. Instead, a group of lenders form a syndicate. These could include:

– Development Finance Institutions (DFIs) (these are also known as “multilateral” banks): these organisations, such as the International Bank for Reconstruction and Development, whose goals are to reduce poverty and promote private investment by making or guaranteeing loans made by the private sector.

– Commercial Lenders: there will usually be a “lead” commercial bank or “lead arranger” who arranges for the syndication of the commercial loan to several banks.

– Term B lenders: these are institutional lenders (such as insurance companies and hedge funds). These lenders are generally more willing to finance riskier projects.

Sponsors

The sponsors are the parties who conceive and carry out the project to satisfy a particular objective, for example, the generation of power. The sponsors are the ultimate equity beneficiaries of the project, whose primary aim is to own a completed, fully operational and (eventually) debt-free project that will maximise returns.

Host governments

A project will often need consent from a host government, particularly if it involves extracting natural resources from that country. In most cases, the government will also have a stake in the project.

Contractors

The contractors are the people who build the project. They are independent from the lenders and the sponsors.

Off-takers

The off-takers are the people who benefit from the project, usually by buying the product the project will produce or otherwise benefiting from it. The government is often the off-taker.

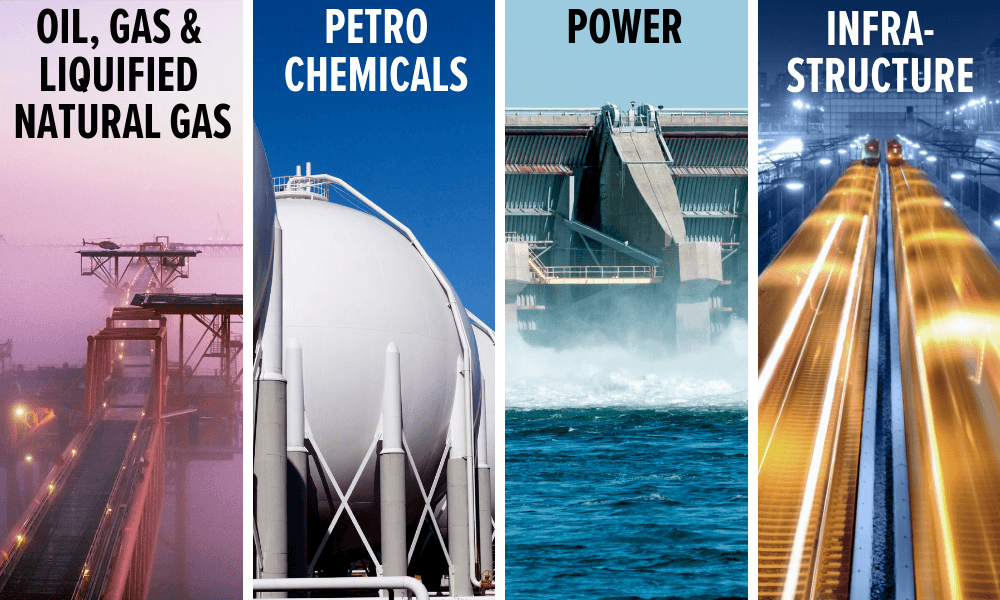

3. KEY INDUSTRIES

• Oil, Gas & Liquified Natural Gas (LNG)

• Petrochemicals – typically chemical products

• Power – renewable, non-renewable and nuclear energy

• Infrastructure – building projects such as railways, roads, stadium, telecoms line etc.

4. REGIONS

Emerging markets are prime locations for project financings with the Middle East and Africa being key regions due to their high levels of natural resources.

As an example, the Project Development & Finance team in Shearman & Sterling’s Abu Dhabi office has seen an increase in work in the last few years, with key clients such as ADNOC making investments in both renewable and non-renewable projects in the region.

5. KEY CONCEPT: RISK ALLOCATION

A successful project can be very beneficial to all the parties involved whether this is financially or through the creation of infrastructure, particularly in developing countries.

The risk involved in project financings however is equally high. Projects span across extended periods of time and are often located in jurisdictions in which a similar project has never been undertaken before and which may not have the necessary infrastructure or framework (legal or otherwise) to see it through without complications.

This lack of certainty inevitably creates a host of risks, such as:

(a) political instability, especially in certain developing countries, where changes in government and regime can be swift and radical;

(b) delay and cost overrun, two issues which are potentially linked as it is not always possible to predict market movements (for example with relation to labour costs or availability of building materials) five or ten years down the line; or

(c) natural catastrophes resulting in the destruction of the infrastructure or rendering the project non-viable (for example the lack of wind in a location where a wind farm is being built).

As the project does not have a revenue stream during its construction phase, the debt can only be repaid during the operations phase, when the project is up and running (there is very little physical security to be taken as a bank will not mortgage a half-built power plant and attempt to repossess it in the event of a payment default).

Some of these risks can be anticipated; project financing deals involve rigorous due diligence and numerous conditions precedent requirements including, amongst others, studies on the environmental and financial viability of the project.

However, a great number of those risks cannot be avoided. A large part of the negotiations between the parties concerns the allocation of such risk between the parties based on which party is best placed to mitigate that risk – for example, the risk of a change in the law that could result in the project being unlawful will usually be taken on by the government.

6. JARGON BUSTER

Upstream

This stage involves the initial search for oil or natural gas and their extraction and production in the oil and gas industry. This is usually achieved through the drilling and subsequent manning of wells in order to bring the oil or natural gas to the surface. The majority of exploration endeavours are offshore, however onshore upstreaming is also possible.

Midstream

This stage involves the transportation of the products once they have been extracted usually from the offshore location they were extracted from. The term is most often applied to the pipeline transportation of crude oil and natural gas but may also be used in relation to the transport of natural gas by LNG vessels.

Downstream

This stage involves the refinement, processing and marketing of products to be used for energy in the oil and gas industry. This, for example, includes the transportation to the end consumers and may also involve trading of the products in the wholesale market.

Special Purpose Vehicle (SPV)

The Project Company through which the project will be carried out is an SPV, i.e. a shell company usually formed as a limited company. The sponsors invest equity into the SPV, which will have the right to carry out the project and operate the assets for a set period under the terms of the concession.

Limited Recourse Financing

The lenders financing a project only have “limited recourse” in the event something goes wrong in the implementation of the project and the sponsors are unable to pay their loan. This is because the Project Company is an SPV, which allows the sponsors to “hide” behind it, as the limited liability nature of the SPV means the sponsors are not personally liable for the money owed to the lenders.

Public Private Partnership (PPP)

This is a range of business structures and partnership arrangements involving the government and the private sector, from private finance initiatives (PFI) to joint ventures and concessions, outsourcing and the sale of equity stakes in state-owned businesses.

Operator

The party responsible for managing and operating the project in accordance with the agreed contract terms.

Suppliers

The project company may have to enter into several contracts with suppliers to get the project going (e.g. in a gas-fired power plant the project company may need to secure access to long-term natural gas.

Technical Advisors

This party analyses the feasibility of the project and its ability to generate revenues required to repay debt to the lenders. Lenders will usually require an assessment from the Technical Advisor before agreeing any financial documents

7. HEADLINE DEAL: SADARA INTEGRATED CHEMICALS PROJECT

Shearman & Sterling advised Dow Chemical Company, one of the world’s largest speciality material companies, on its joint venture with leading energy supplier Saudi Arabian Oil Company (Aramco) for the construction and operation of the USD 20 billion Sadara Chemical Project.

The project was located in Al Jubail, Saudi Arabia and is said to be the largest ever industrial project in history, comprising 26 plants, the final of which was commissioned in 2017.

8. TRAINEE OVERVIEW – PROJECT DEVELOPMENT & FINANCE

Watch this video to hear one of our trainees give an overview of the Project Development & Finance practice and explain the type of work trainees typically carry out during their time in the department.